China Inc. Has The West In A Strategic Metals Stranglehold

On Wednesday, Axios published comments from a top CIA official who declared that “China is the existential threat to American security in a way we really have never confronted before.” Deputy Director Michael Ellis also said his agency’s top priorities were to help the US maintain a “decisive technological advantage” in several areas, including AI, batteries, biotech, and computer chips.

Ellis said that the CIA is being restructured to deal with threats from China. It aims to hire more skilled people, including “more people with technical backgrounds...more STEM grads.” While America’s top spy agency is focusing on AI, batteries, and chips, China has spent the past three decades cornering the market on the metals, minerals, and other commodities needed to fabricate and mass-produce those very same technologies.

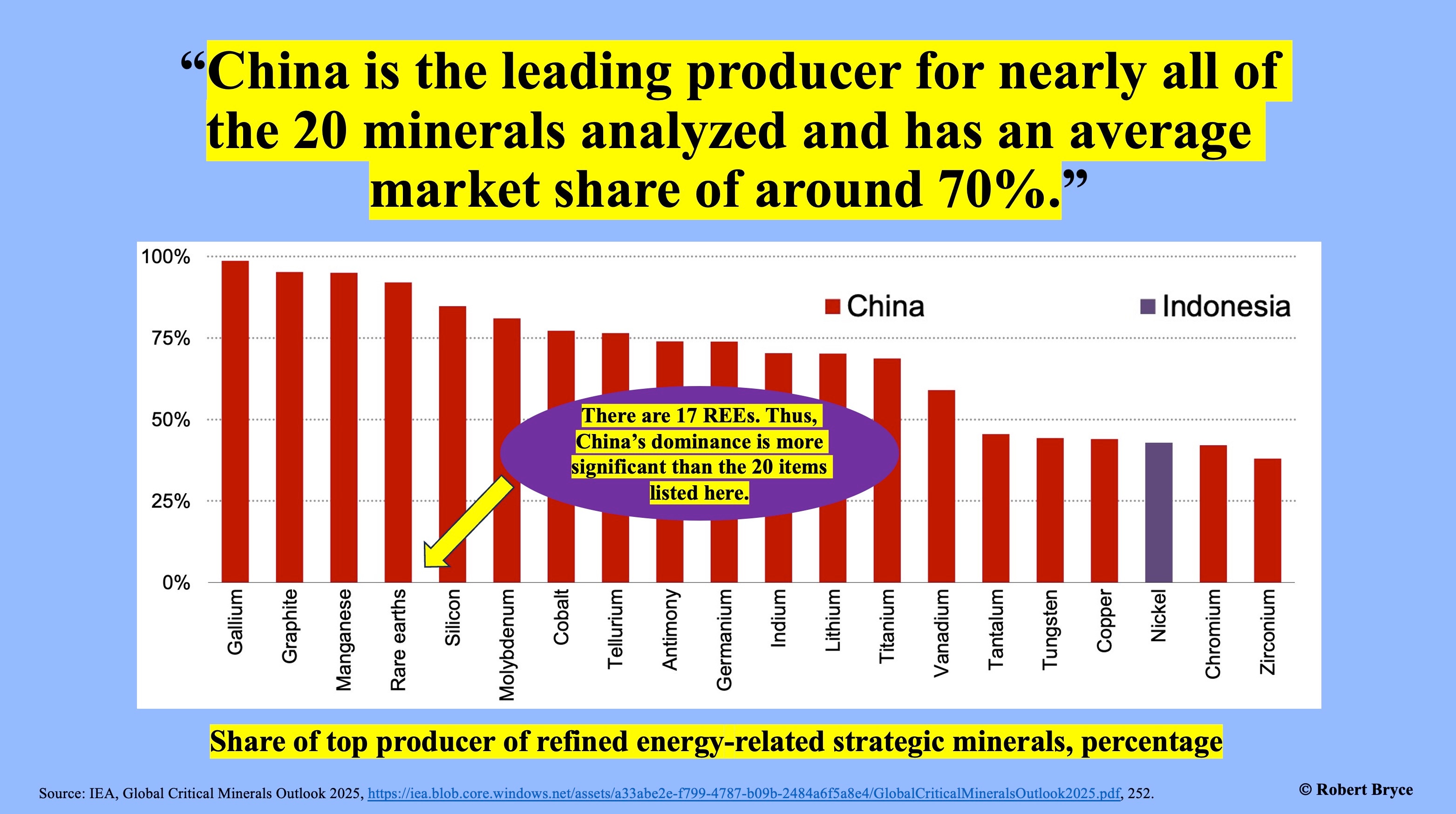

Ellis’ comments were published the same day the International Energy Agency released its Global Critical Minerals Outlook 2025. And the findings of that report are a sobering reminder that China has a near-monopoly on numerous key commodities. The IEA found that “China is the dominant refiner for 19 of the 20 minerals analyzed, holding an average market share of around 70%.” However, even that figure understates China’s dominance because it lumps all the rare earth elements (REEs) into a single line item. In reality, China’s grip is even tighter.

The IEA pays particular attention to the escalating trade war, which has led China to restrict the export of dozens of items. Here’s the key passage:

In a world of high geopolitical tensions, critical minerals have emerged as a frontline issue in safeguarding global energy and economic security. The wave of recent export restrictions highlights the strategic urgency of strengthening the resilience and diversity of critical mineral supplies as the world moves towards a more electrified, renewables-rich energy system. (Emphasis added.)

While the IEA pleads for “strategic urgency,” the facts show China’s grip on the commodities needed to produce computer chips, batteries, EVs, wind turbines, and other high-tech products is only tightening. Beijing is ratcheting export restrictions on everything from antimony to yttrium, and Western manufacturers are starting to feel the pain.

Here’s a deep dive into the new IEA report, with 10 charts.

China’s export restrictions on key industrial metals are having significant impacts on US manufacturers. On Thursday, I spoke to a friend who leads a large company that makes lead-acid batteries. His company has had to raise the price of its forklift batteries by more than 12% in the last six months alone. Why? Deep-cycle lead-acid batteries like those used in golf carts and forklifts, require significant amounts of antimony. As I noted last December in “China Runs The Table,” China has banned the export of three strategic elements — antimony, gallium, and germanium — to the US.

China produces about 75% of the world’s antimony the US has been importing more than 60% of its antimony from China. But the country’s export ban has sent antimony prices skyward. Fifteen months ago, my friend’s company paid about $6 per pound of antimony. At the end of April, the spot price was $26 per pound. My friend reminded me that antimony is a key commodity used in munitions. The element (Sb on the Periodic Table) is critical to producing tungsten steel and hardening lead bullets and armor-piercing munitions. “I know the government is very concerned,” he said. “What they are doing, I don’t know.” (Gallium and germanium are used in the production of semiconductors.)

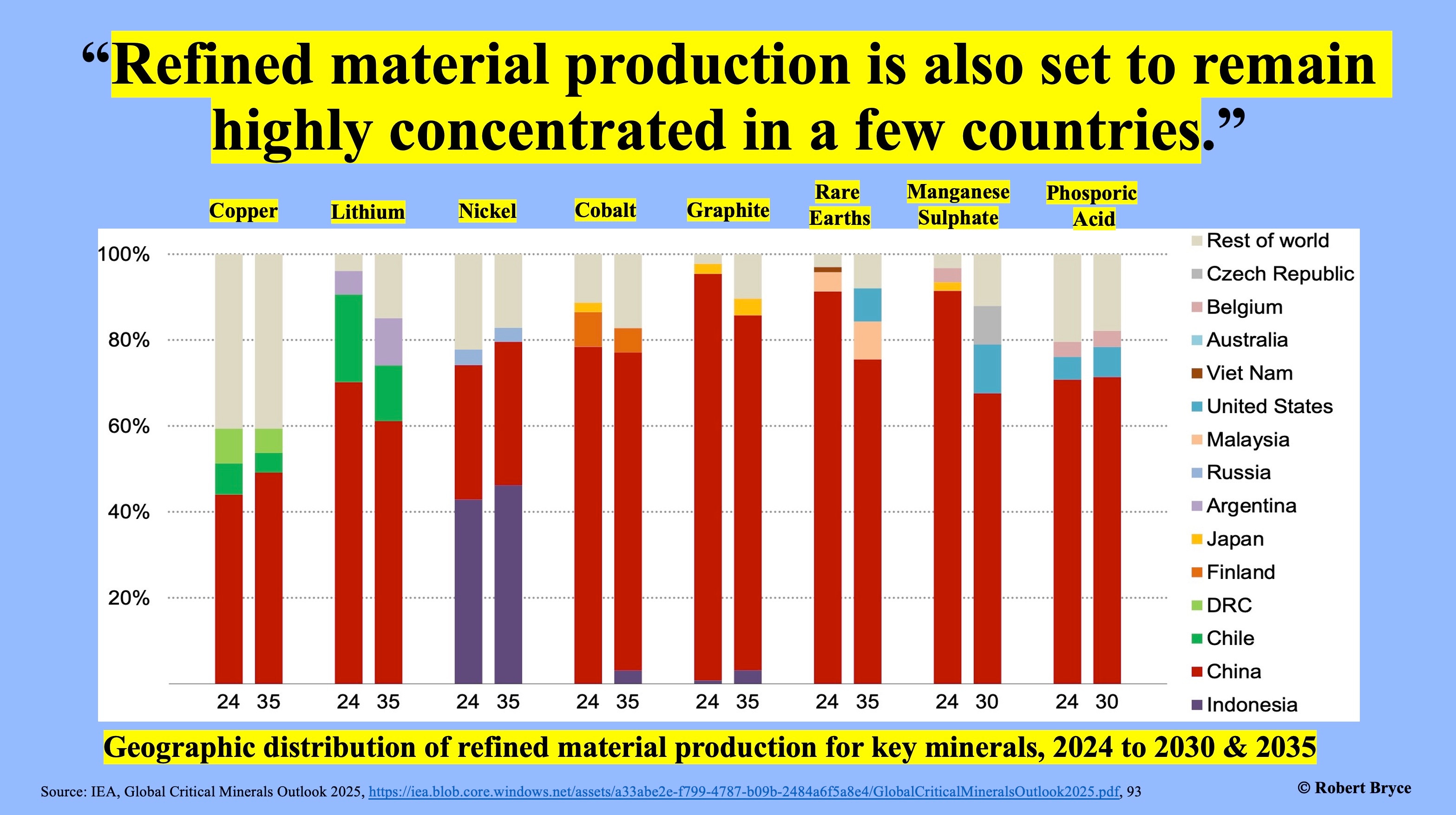

The IEA’s report is more than 300 pages long. The chart above may be the most important graphic in the entire document, as it shows China’s near-monopoly on 20 key industrial commodities. But the chart doesn’t appear until page 252. In journalism, we call that “burying the lede.” Note that most of the 20 items shown are metals. Graphite is not a metal. It’s a naturally occurring crystalline form of carbon that is an essential ingredient in lithium-ion batteries. Silicon, tellurium, antimony, and germanium are all metalloids, meaning they have properties intermediate between metals and nonmetals.

While the chart provides a powerful illustration of China’s dominance, it also understates its market power. The chart shows just one entry for rare earths. That’s an error. There are 17 REEs, including the 15 lanthanides plus scandium and yttrium. Thus, a more accurate count shows that China is the leading producer of 35 out of the 36 minerals the IEA analyzed! For perspective, the Periodic Table has 118 elements. Thus, China has a headlock on nearly 30% of all elements.

Subscribed

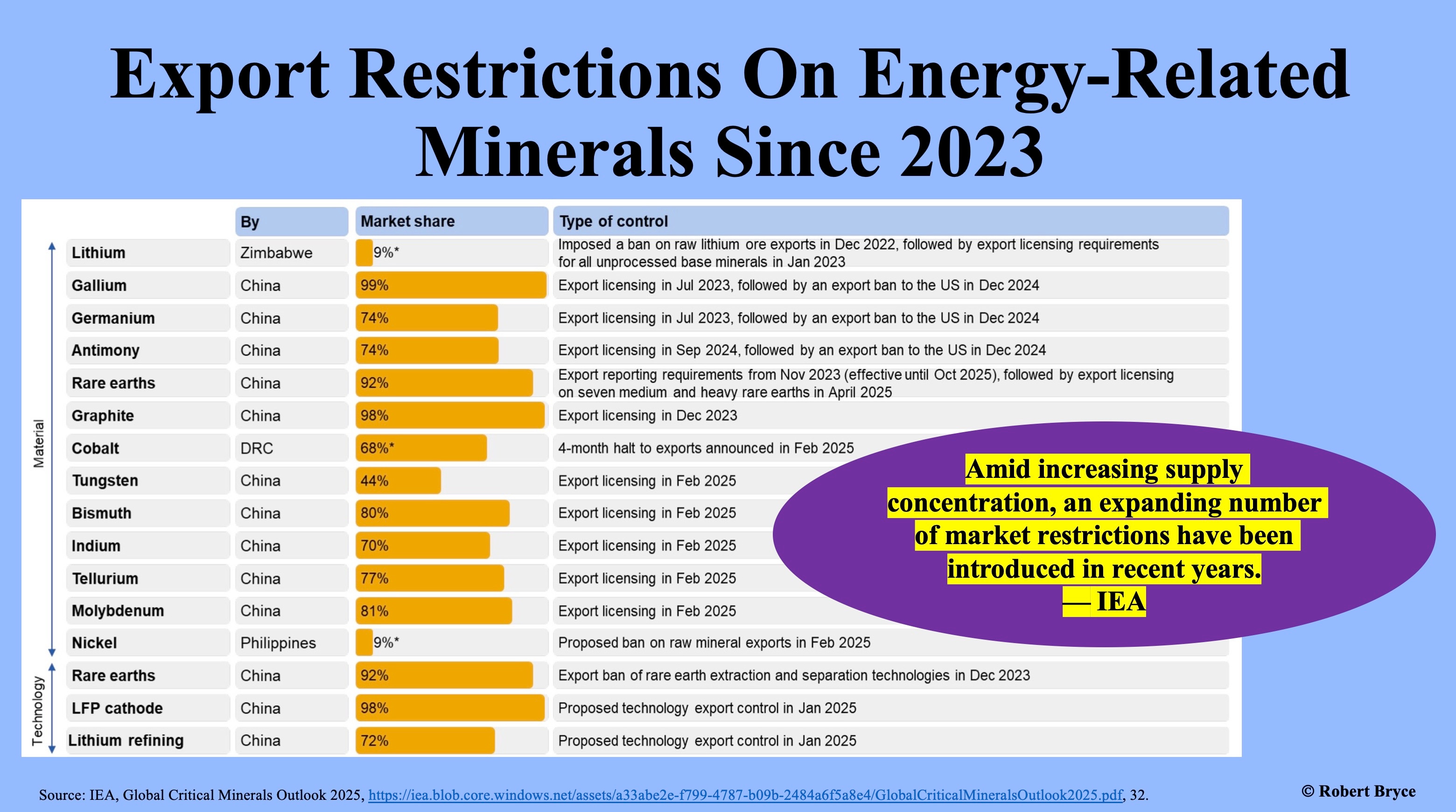

The chart above includes another graphic from the IEA report. As you can see, China has been imposing export restrictions on key industrial commodities since 2022 and it began imposing more controls in February in response to President Trump’s tariffs.

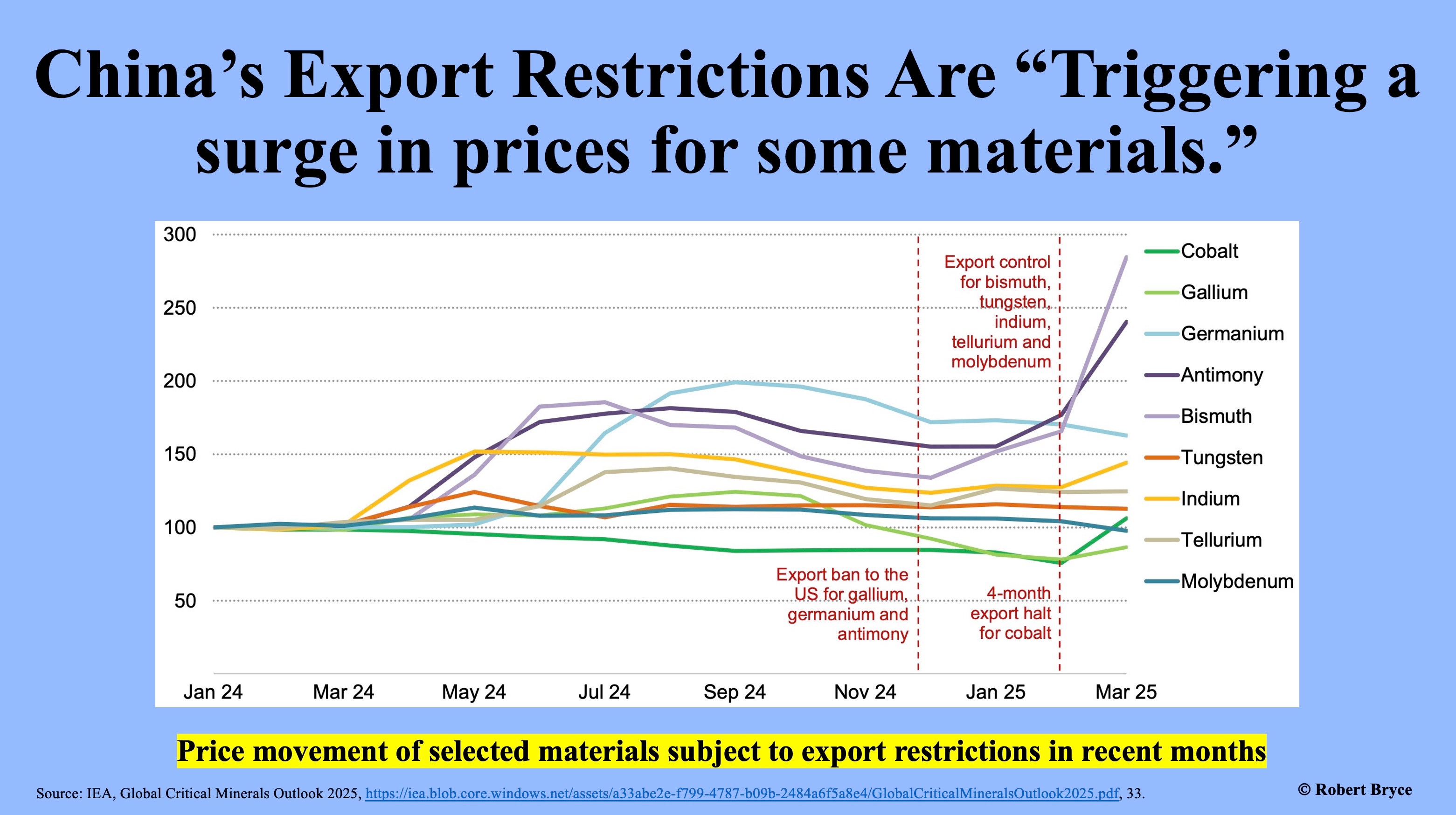

The export restrictions have resulted in price increases for several materials, including antimony. As seen above, the only element that has surged in price more than antimony is bismuth, which is used as a propellant in rockets, munitions, semiconductor manufacturing, and metal alloys in defense applications. The US imports 100% of its bismuth. According to the US Geological Survey, about 68% of those imports have been from China.

Subscribed

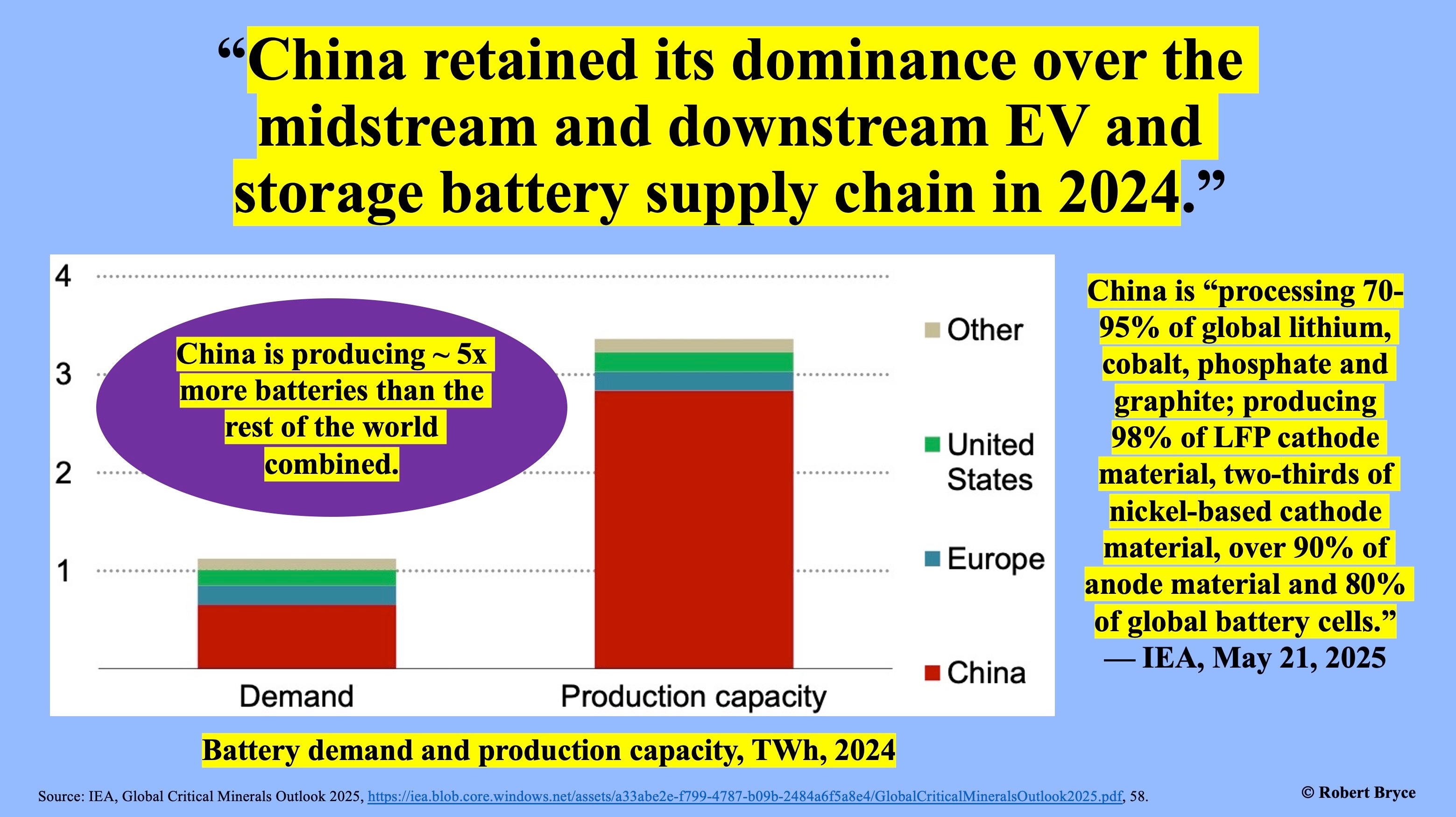

The deputy director of the CIA said he wants the US to have a technological advantage on batteries. However, as seen above, China now produces about five times more batteries than the rest of the world combined.

China’s battery production capacity depends on supplies of key metals, including copper, lithium, nickel, and cobalt. As seen above, China’s share of the refining capacity for some of those metals, particularly copper and nickel, will increase over the next decade or so.

REEs, also known as the “green” elements, are critical ingredients in a myriad of weapon systems, high-strength permanent magnets, electric vehicles, wind turbines, and numerous consumer goods. I began writing about China’s dominance of REEs in my fourth book, Power Hungry: The Myths of “Green” Energy and the Real Fuels of the Future. And it was clear back in 2010 what China was planning to do.

I noted that China controlled between 95 and 100% of the global supply of REEs. I explained that REEs are essential ingredients in neodymium-iron-boron (NdFeB) magnets and that those magnets are a key chokepoint in the development of the “green” economy.” I also noted that China was beginning to restrict exports of REEs and that it could use them as a weapon in any trade conflict. I wrote:

The availability of rare earths is not just about balance of trade, it’s also about national security. The US military is heavily reliant on high-tech weaponry, which means navigation systems, guidance systems, radios, and computers – all of which require rare earths. Now, suppose that the US decides to impose trade sanctions on China, perhaps due to some type of dispute over carbon emissions. What might China do in retaliation? Well, one obvious way to retaliate would be to cut off the flow of rare earths to the US and other countries, thus pinching the US Defense Department’s ability to obtain the high-tech equipment it needs. China’s near-monopoly control of the green elements likely means that most of the new manufacturing jobs related to “green” energy products will be created in China, not the US. (Emphasis added.)

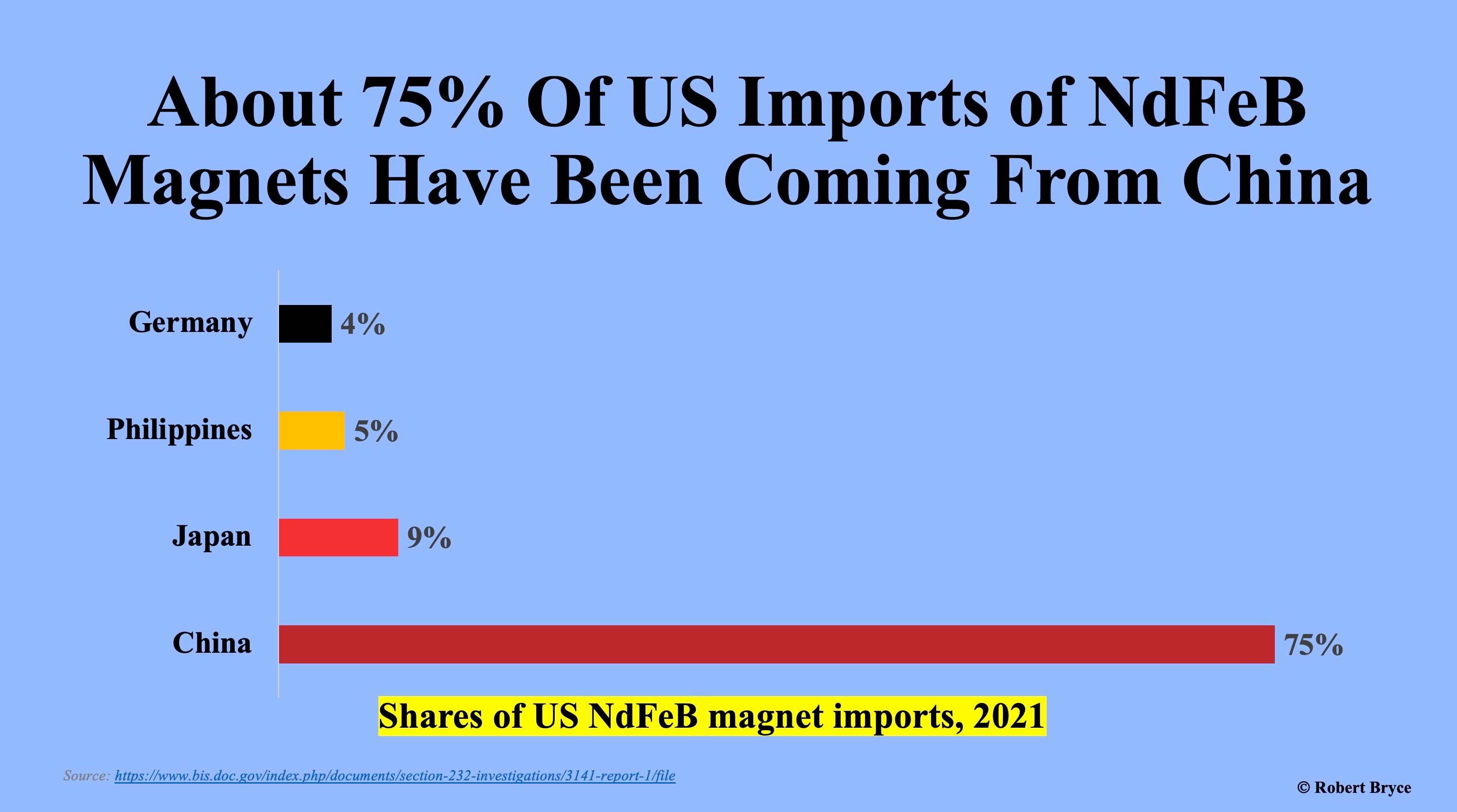

In 2023, in a piece titled “The EPA’s China Syndrome,” I explained that China was planning to ban the export of technologies used to process and refine REEs and that the Commerce Department had determined that dependence on REE imports threatens to “impair the national security” of the US. The same 2022 Commerce Department report also found that in 2021, the US imported about 75% of its NdFeB magnets from China.

Subscribed

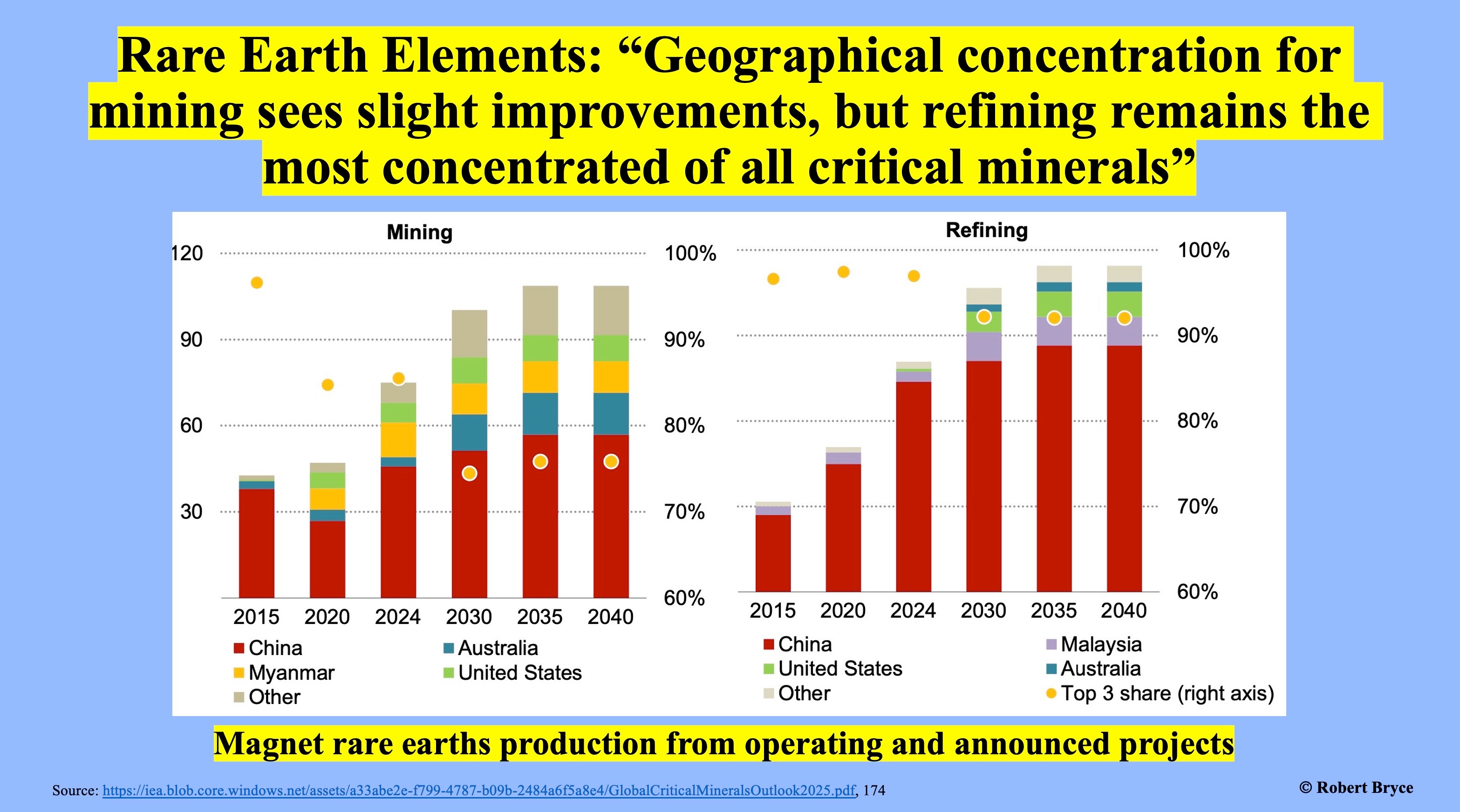

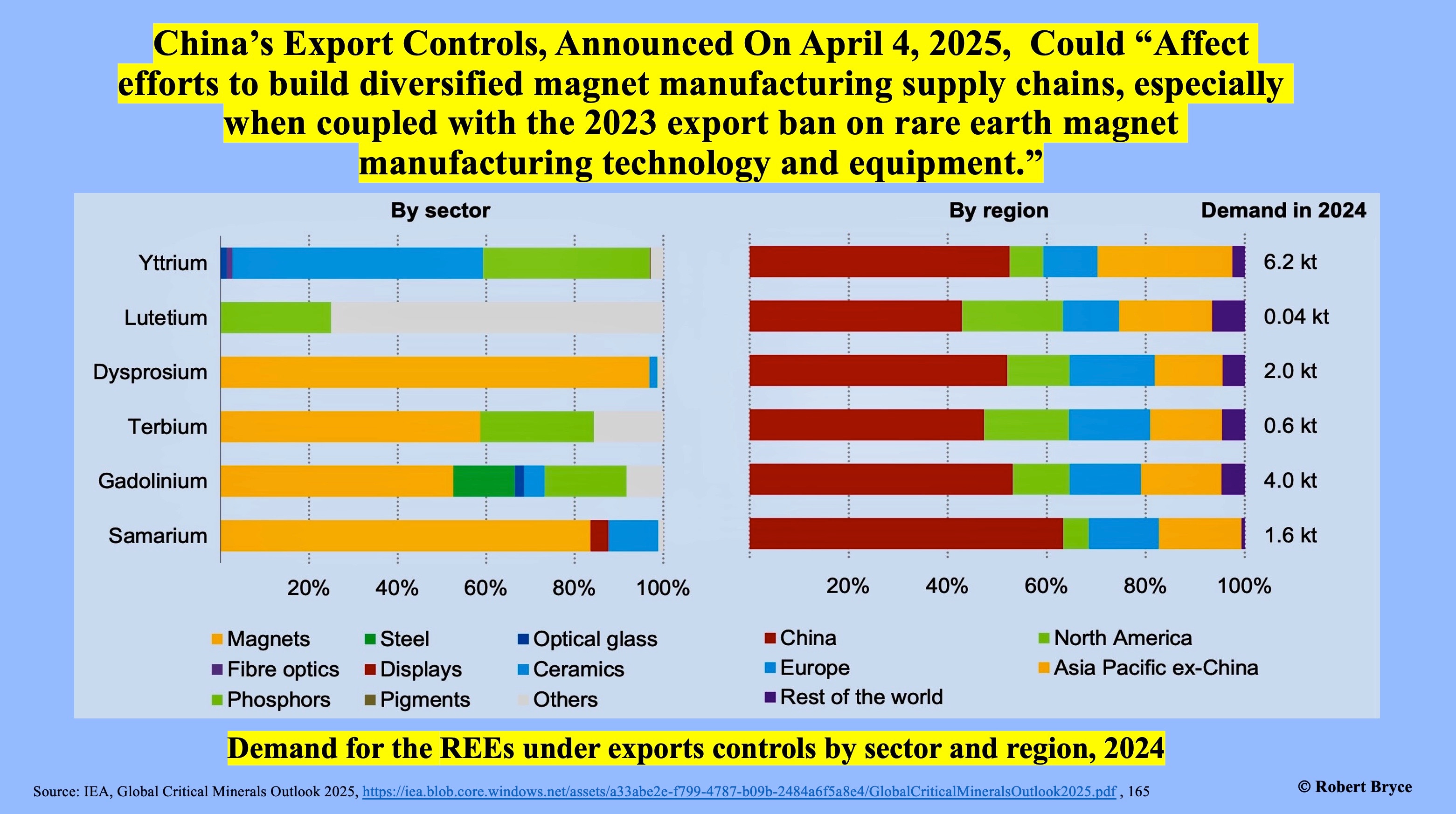

The new IEA report put a special focus on REEs. As seen above on the left, dysprosium, terbium, gadolinium, and samarium are critical ingredients in high-strength magnets. The image on the right shows that China consumes as much as 60% of its REEs.

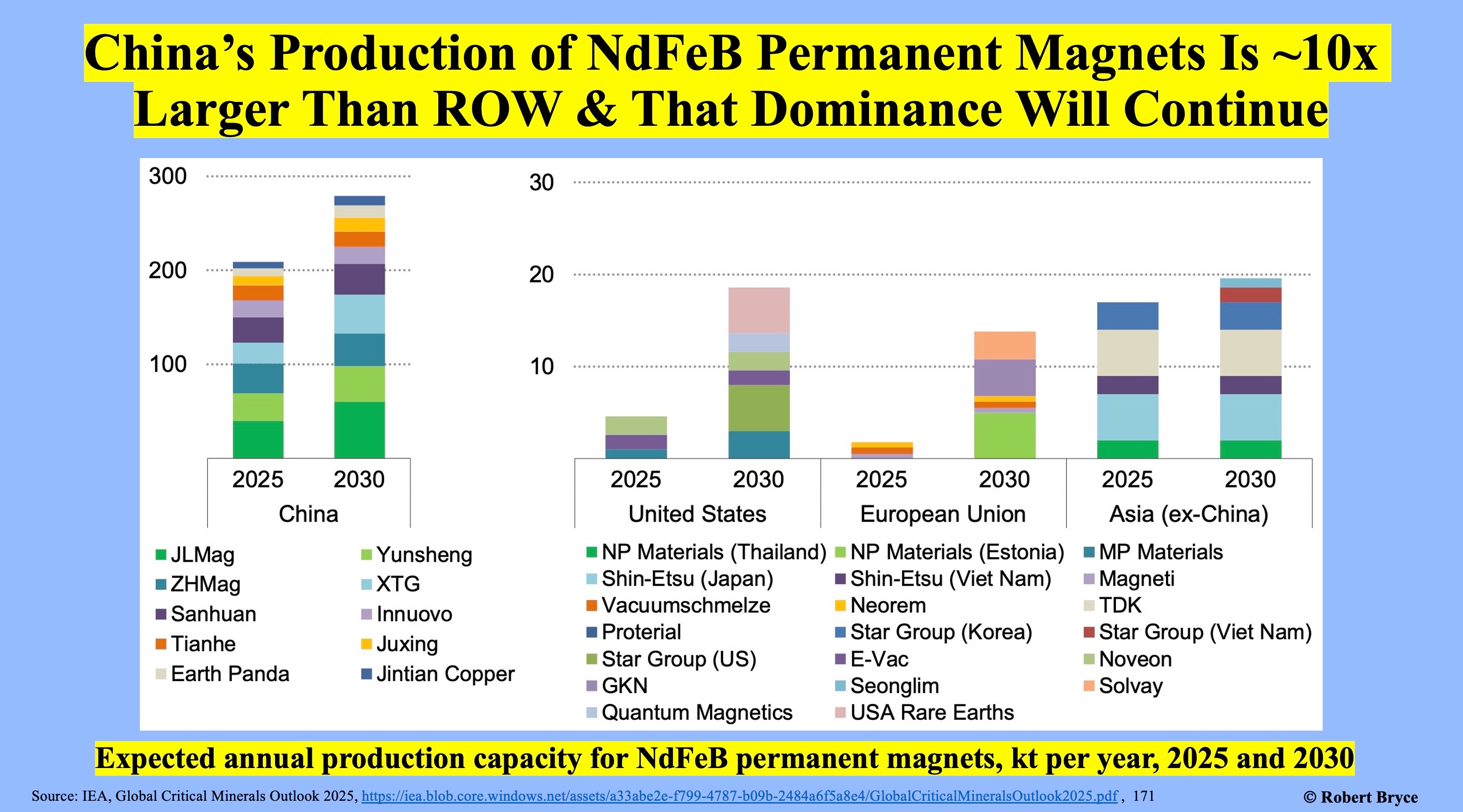

A chart on page 171 of the IEA report shows that China has a near-monopoly on NdFeB magnets and that despite efforts by other countries to ramp up production, by 2030, China magnet production capacity will likely still be more than five times larger than that of the rest of the world combined.

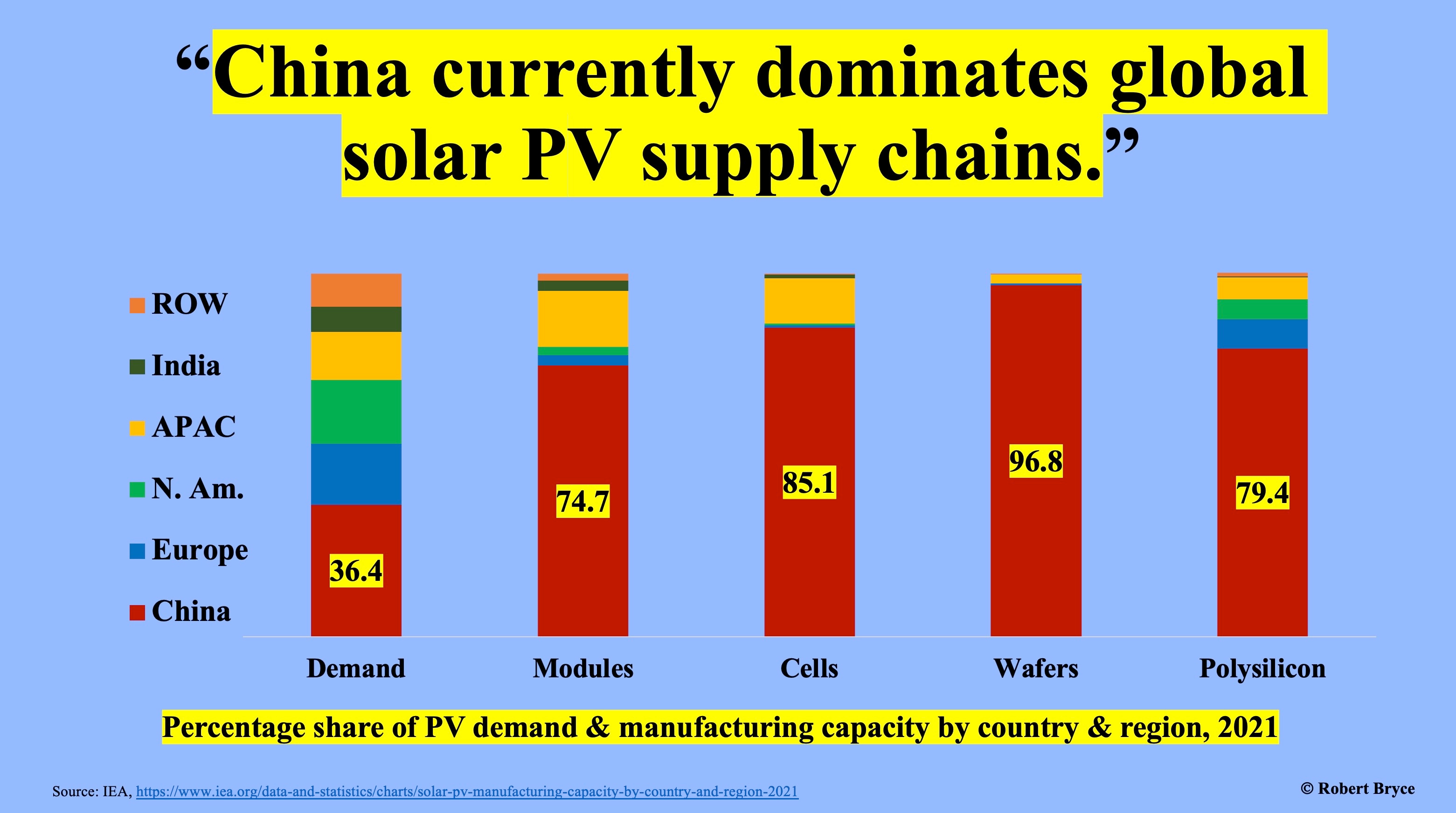

Although the IEA’s report doesn’t spend much time looking at solar energy, it’s abundantly clear that China also has a stranglehold on solar supply chains. The above chart comes from a 2022 IEA report. Unfortunately, little has changed since that report came out. In 2023, a German agency estimated that China controlled 83% of the global market for polysilicon. It’s worth recalling that solar panels are a prime symbol of the renewable energy fetishism that dominates today’s debates over climate change and climate policy.

Furthermore, the lavish federal subsidies for solar energy in the US may soon come to a screeching halt. As Energy Bad Boys — Isaac Orr and Mitch Rolling — explained in a Substack on Saturday, Congress is poised to roll back the solar subsidies included in the Inflation Reduction Act of 2022. They explain that the latest version of a massive reconciliation bill (a pdf of the legislation is 1,118 pages!) that is now heading to the Senate “includes provisions that bar US projects from using components, subcomponents, or even materials from China” and that would then “make it nearly impossible for US solar and battery manufacturers to qualify for the tax incentives” that were previously available.

I’ll conclude by noting that the legislation dubbed the “One Big Beautiful Bill Act” has not become law. Furthermore, if the bill does become law in its current form, the measures prohibiting the use of Chinese components will only impact a fraction of the commodities that China exports to the US and other Western countries.

IEA report again shows that the US and other Western countries are painfully dependent on a powerful geopolitical adversary for a panoply of critical metals, metalloids, and industrial commodities. CIA officials can label China an existential threat until the cows come home, but it’s also clear that the US has sleepwalked into a supply chain calamity. From copper and nickel to bismuth and batteries, the US needs what China is selling, and that will be true for decades.

As my friend in the battery business told me last week, “When it comes to minerals, China has us right where they want us.”

Media Hit

On Friday morning, I recorded a podcast with fellow Substack writer, The Contrarian Capitalist. We discussed the four executive orders on nuclear energy I wrote about last Tuesday (our conversation took place a few hours before Trump signed those orders), the UK’s energy foolishness, the $10,000 Question, China, India, and “a global tour of energy.” It was fun. Have a listen.

Subscribed

Speaking Inquiries

A friendly reminder: I make my living as a professional speaker. I have 33 engagements on my calendar this year. Next month, I will be in Australia for a multi-city speaking tour sponsored by the Institute of Public Affairs. I’ll be talking about Australia’s energy sector and its net zero madness. If you need a speaker for an upcoming event, please get in touch. If you want to see me in action, have a look at my YouTube page.

Comments

Post a Comment